Buying a House With Credit Card Debt: First-Time Buyer Tips

💭 Why This Feels Overwhelming (And You’re Not Alone)

If you’re renting right now and dreaming of buying your first home, chances are one big thing keeps holding you back: credit card debt.

You’re not the only one. U.S. households carry over $1 trillion in revolving debt (mostly credit cards). It’s no wonder so many first-time buyers think:

- “I can’t buy until I’m debt-free.”

- “My credit score isn’t good enough for a mortgage.”

- “I’ll never save a down payment while paying so much interest.”

The truth? Yes, debt matters, but it doesn’t have to stop you. With the right approach, you can reduce balances, improve your credit profile, and become mortgage-ready faster than you might expect.

🚧 The 5 Most Common Blockers for First-Time Buyers

- Credit card debt → High balances push up your debt-to-income ratio (DTI) and hurt your credit utilization.

- Down payment myths → You don’t need 20% down. Many loan programs allow 3–5%.

- Credit score fears → You don’t need a perfect 760+. Many buyers qualify with 620–680.

- Income and DTI confusion → Lenders want your DTI (debts ÷ gross income) below ~43%.

- Market timing paralysis → Waiting for the “perfect time” can keep you renting forever.

💳 How Credit Card Debt Affects Your Mortgage

Lenders care about two main things when it comes to revolving debt:

- Credit utilization ratio → How much of your available credit you’re using.

- Example: $3,000 balance on a $10,000 limit = 30% utilization.

- Under 30% = good. Under 10% = excellent.

- Debt-to-income ratio (DTI) → Lenders calculate this from your minimum payments, not your balances.

- Example: $6,000 gross monthly income, $180 in card minimums, plus car and student loans = ~13% DTI before adding a mortgage.

- A $2,000/month mortgage could push that to 46%, above most lender limits. Lower balances = lower DTI.

📋 Action Plan: Budget + Payoff Strategy

The fastest path is simple:

- Decide your monthly budget for extra debt payments.

- Pick your payoff strategy:

- Snowball: focus on the smallest balance first for quick wins.

- Avalanche: focus on the highest interest rate first to save the most money.

- Stick to the plan month after month.

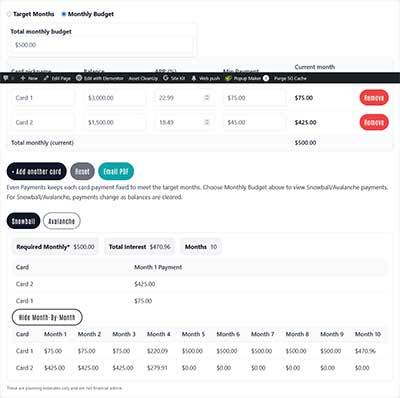

👉 Want to see exactly how your balances, minimums, and timeline look? Use my Multi Credit Card Paydown Planner Tool to generate a personalized month-by-month payoff plan.

⚡ Quick Wins That Boost Your Profile

- Stay under 30% utilization per card (lower is better).

- Pay before the statement date so lower balances are reported.

- Remove authorized user accounts if someone else’s debt inflates your DTI.

- Don’t close old cards, that can shrink your credit history.

⏳ Timeline Scenarios: 3, 6, and 12 Months

- 3 months → Lower utilization under 50%, no late payments, documents organized.

- 6 months → Balances under 30% utilization, DTI below 40%, credit score +20–40 points.

- 12 months → Major balances paid down, cash savings built, strong position for pre-approval.

🧐 Myths vs Facts

- Myth: You need 20% down.

✅ Fact: First-time buyer loan programs allow as little as 3%. - Myth: Closing credit cards boosts your score.

✅ Fact: It often hurts, since it lowers available credit. - Myth: Any debt disqualifies you.

✅ Fact: Manageable debt within DTI guidelines is acceptable.

✅ Checklist to Talk to a Lender With Confidence

- W-2s or tax returns (2 years)

- Recent paycheck stubs

- Bank statements

- List of debts with balances + minimums

- Know your DTI (aim ≤43%)

- Savings target (down payment + closing costs)

📌 Do This Next (6 Steps)

- Pull your free credit reports.

- List every balance, limit, and minimum.

- Decide your extra monthly payoff budget.

- Choose Snowball or Avalanche.

- Track your DTI progress.

- Reach out to a lender when you’re under 43% DTI.

💌 Warm Encouragement

You don’t need to be debt-free to buy a home, you just need to be in range. Every payment you make today is building tomorrow’s opportunity.

Want to see a clear month-by-month plan? Try my Multi Credit Card Paydown Planner Tool and email yourself a copy. It’s the easiest way to go from “stuck with balances” to “mortgage-ready.”