Renting vs Buying

What if that same payment could start building your future instead of someone else’s?

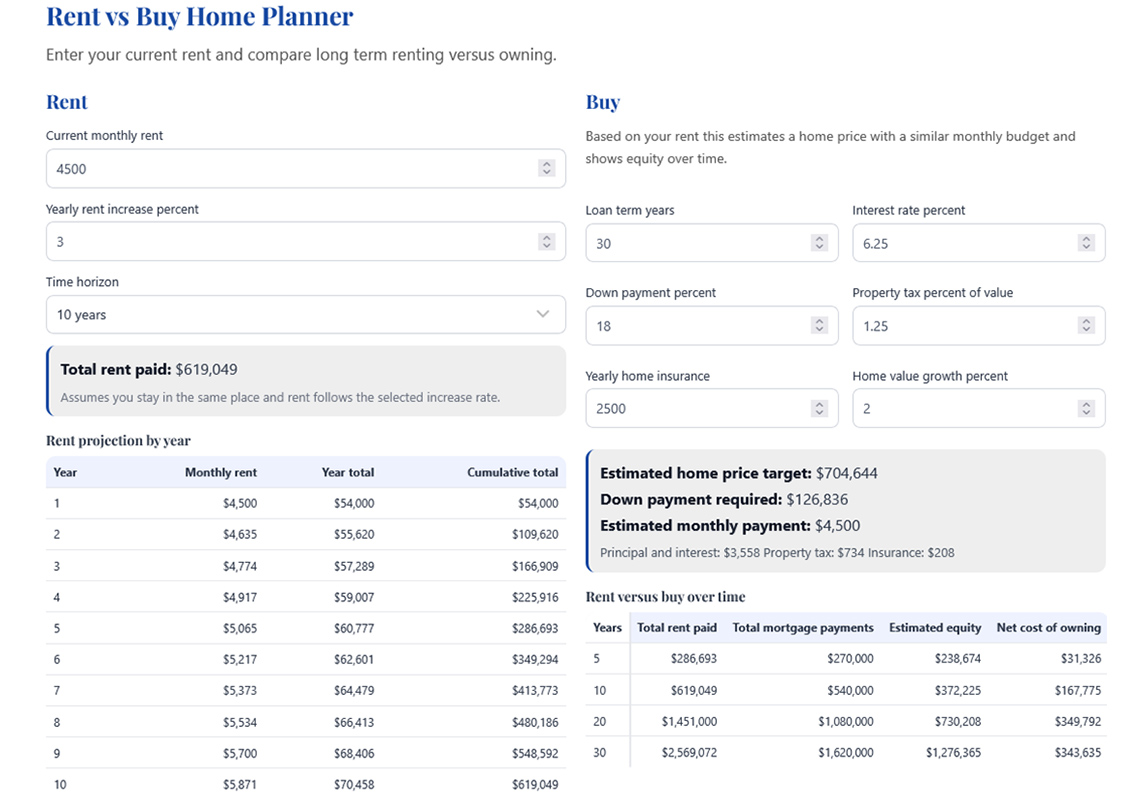

Use this tool to see how much home your current rent could buy, how your payments stack up over time, and how equity grows when your money starts working for you.

Rent vs Buy Home Planner

Enter your current rent and compare long term renting versus owning.

Rent

Rent projection by year

| Year | Monthly rent | Year total | Cumulative total |

|---|

Buy

Based on your rent this estimates a home price with a similar monthly budget and shows equity over time.

Rent versus buy over time

| Years | Total rent paid | Total mortgage payments | Estimated equity | Net cost of owning |

|---|

Rent vs Buy Home Planner Notes

Down Payment

Your down payment is the amount of money you pay upfront when you buy a home. The 18% down payment shown in the calculator is just an example, it’s not meant to discourage you, but to help you see what a more traditional scenario looks like. Every situation is different, and with the right guidance, you might need far less to get into a home of your own.

The down payment includes your earnest money deposit and closing costs.

The earnest money deposit is a small amount of money you put down when you make an offer on a home to show the seller you’re serious. It’s usually applied toward your down payment or closing costs at the end of the deal.

Closing costs are the fees and expenses that come with finalizing a home purchase, things like lender fees, title insurance, escrow, and appraisal costs.

There are loan programs for first-time home buyers that can lower the down payment, sometimes even below 5%. Also, closing costs are sometimes negotiable, meaning the seller or lender might cover part of them. I’d be happy to connect you with a trusted loan officer who can go over those options and help you see what’s realistic for your budget.

Home Value Growth Percent

How much your home’s value is expected to go up each year. It’s an estimate of appreciation, the rate at which your home might increase in value over time. This percentage is influenced by market conditions like supply and demand, interest rates, and the local economy, so it can fluctuate.

Estimated Equity

How much of your home you truly own after subtracting what you still owe on your mortgage. This number also factors in how much your home’s value might rise over time based on the Home Value Growth Percent you set. In simple terms, it shows how your equity can grow as you pay down your loan and your home’s value goes up.

Net Cost of Owning

What buying really costs you after accounting for the equity you’ve built. It’s like asking, “How much did I truly spend once I subtract what I’ve gained in home value?” If this number ends up being negative, that’s actually a good thing, it means your home’s value and equity have grown so much that they’re worth more than what you’ve paid out. In other words, your investment has made you money instead of costing you.

Why HOA fees aren’t included in the Rent vs Buy tool

HOA fees can be very different from one neighborhood to another, and they aren’t tied to the price of the home. Because they vary so much, this calculator leaves them out. If the home you’re considering has an HOA, just add that monthly amount to the estimated payment shown here.

Mortgage Estimate

Run the numbers and see what fits your budget. A quick way to understand monthly payments before you decide.

Rate Comparison

See how different interest rates change your monthly payment, and weigh “buy now vs. wait,” since falling rates often push prices higher.

Renting vs Buying

See how much home your current rent could buy, how your payments stack up over time, and how your money starts working for you.

Plan With Confidence

Numbers are just the starting point. If you’d like a clearer picture of what you can afford, including your personalized loan rate, loan options, closing costs, and down payment strategies, I’m happy to connect you with trusted local lenders.

Want help turning these numbers into a real plan? Let’s talk about your next move.

Mortgage Interest Rates. Updated Daily.

Below are current market averages for home loan interest rates. Rates are provided by Mortgage News Daily.