How Interest Rates Affect Your Buying Power

When you’re shopping for a home, one number can dramatically shape your journey: the interest rate. It’s easy to focus on the home price, but the interest rate on your mortgage determines how much you actually pay over time, and more importantly, what you can afford today.

Let’s break it down in a way that’s easy to understand, so you can make confident decisions as a buyer in any market.

💡 What Is “Buying Power”?

Buying power refers to how much home you can afford based on your income, down payment, and current interest rates. Think of it as your financial reach in the real estate market. When interest rates are low, your buying power stretches further. When rates rise, the same monthly payment buys you less home.

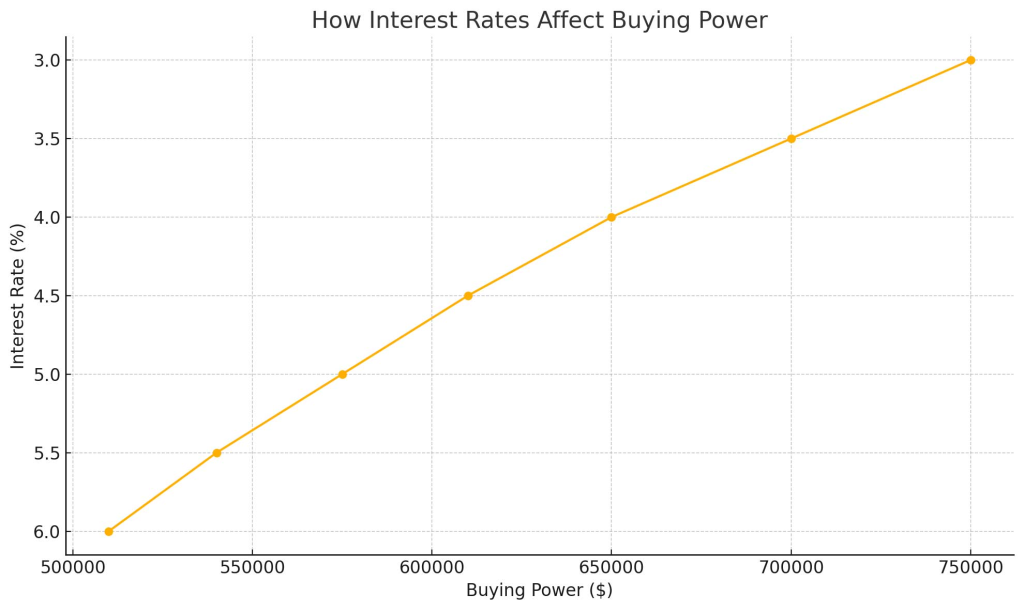

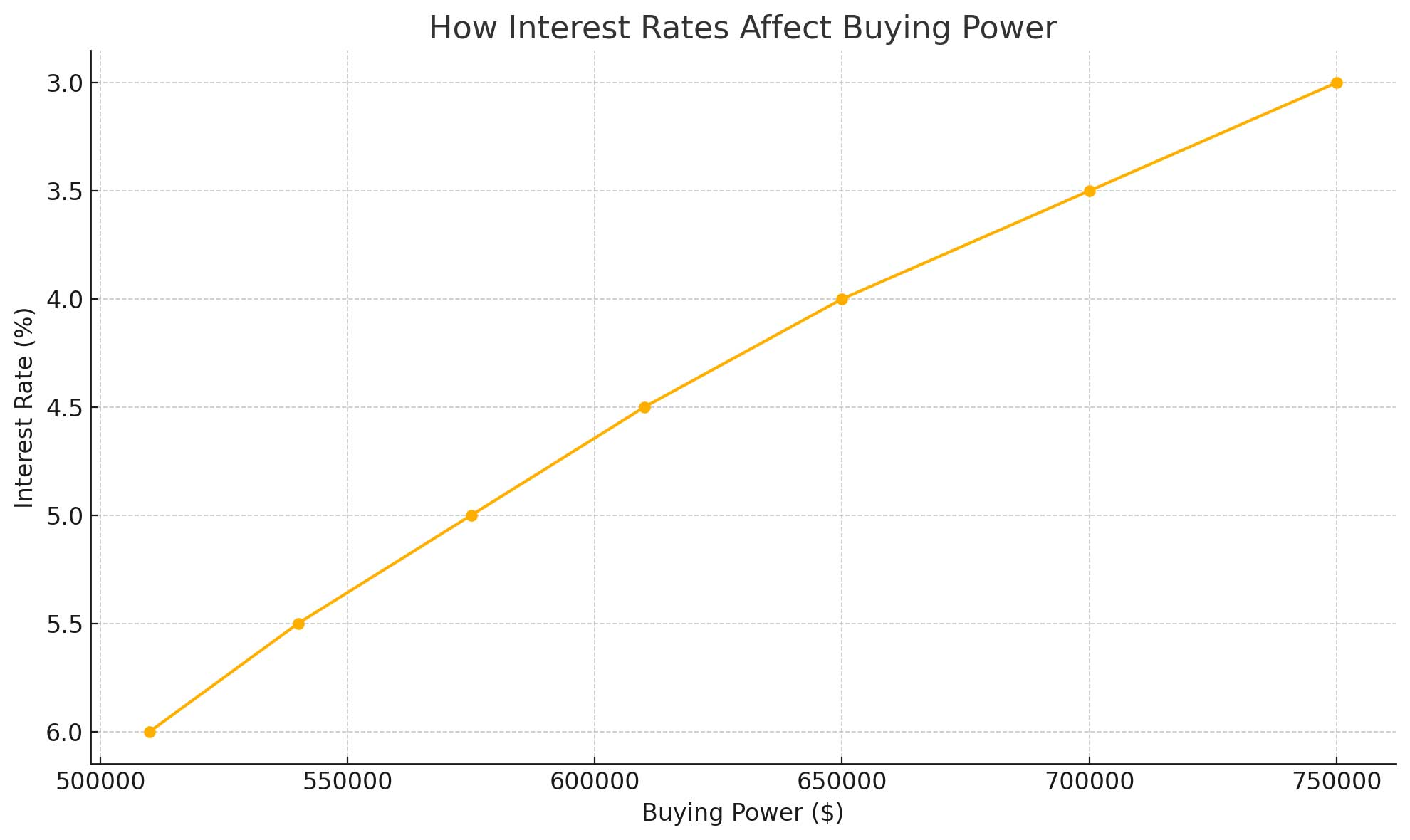

📈When Interest Rates Go Up, Your Budget Shrinks

Let’s say you’re comfortable with a monthly mortgage payment of $3,000. With a 4% interest rate, that might afford you a $700,000 home. But if the rate jumps to 7%, that same $3,000 might only stretch to a $550,000 home.

Why? Because more of your monthly payment is now going toward interest, not the loan principal.

📉When Interest Rates Go Down, You Can Afford More

Conversely, when interest rates drop, your purchasing power increases. You might be able to afford a larger home, one in a better neighborhood, or one with the extra space you need, all while staying within your monthly budget.

🔄 Even a Small Change Makes a Big Difference

Here’s a quick look at how a change in interest rates can impact a 30-year fixed mortgage:

| Interest Rate | Loan Amount | Monthly Payment (Approx.) |

|---|---|---|

| 3.0% | $600,000 | $2,530 |

| 4.0% | $600,000 | $2,864 |

| 5.0% | $600,000 | $3,220 |

| 6.0% | $600,000 | $3,598 |

🧠 The Emotional Side of Buying Power

It’s not just about math. When rates are high, buyers can feel discouraged or hesitant. That’s totally normal. But here’s what’s important: timing the market perfectly is nearly impossible. What you can control is your budget, your goals, and having a smart plan that adjusts to the market.

🏡 What Should You Do as a Buyer?

- Get Pre-Approved Early

Know where you stand before rates move again. A lender can help you understand what monthly payments look like at different price points and rates. - Work with a Real Estate Agent Who Tracks the Market

As your local agent, I can help you stay ahead of market shifts and find properties that match both your lifestyle and your financial comfort zone, no matter where rates stand. - Don’t Wait for “Perfect” Conditions

Buying a home is rarely about the perfect interest rate, it’s about the right home for your needs, at the right time in your life.

🎯Final Thought

Interest rates will rise and fall. But if you’re serious about homeownership, the key is understanding how those rates affect you, and how to move forward confidently, with a plan that works.

If you’re ready to explore your options or just want to talk through what’s possible in today’s market, I’m here to help.