Should You Buy a Home All Cash? Pros, Cons & What Happens Next

What Does It Really Mean to Buy a Home All Cash?

Making an all cash offer is one of the strongest moves you can make in real estate. When a buyer offers to pay the entire purchase price upfront, with no mortgage, it signals certainty, speed, and financial strength.

But buying with all cash isn’t always the end of the story. In fact, many buyers take strategic financial steps after closing. We’ll break that down, and also cover what you can do if you’re not quite in all-cash territory.

✅ Pros of Buying a Home with All Cash

- Faster closings (7–14 days vs. 30–45)

- No mortgage interest or lender fees

- No appraisal required by a lender

- Stronger offer in competitive markets

- Increased negotiation power

❌ Cons of Paying All Cash

- Your capital is tied up in a non-liquid asset

- No mortgage interest deduction

- Potential opportunity cost

- Reduced financial leverage

📑 Do You Still Sign Forms in an All-Cash Deal?

Yes, even without a mortgage, you’ll still need to:

- Sign the purchase agreement (RPA)

- Complete all seller disclosures

- Open escrow and verify title

- Pay closing costs (albeit lower without loan fees)

- Sign final closing documents

- Record the grant deed to officially own the home

In California, cash doesn’t bypass the need for escrow or title services, but it does make the path smoother.

🔄 What Smart Buyers Do After Closing on an All-Cash Purchase

Paying all cash gives you a clean slate, but it also opens up strategic opportunities. Here’s what savvy buyers often do next:

1. 💸Take Out a HELOC (Home Equity Line of Credit)

Tap into the home’s value by opening a flexible credit line secured by your property.

- Useful for: renovations, investments, emergency liquidity

- Only pay interest on what you use

2. 🏦Do a Cash-Out Refinance

Refinance the home and take out a lump sum of equity, essentially putting a mortgage on the home after the fact.

- Locks in a fixed-rate mortgage

- Allows you to regain access to capital while still owning the home

3. 📈 Use the Home as Collateral

A free-and-clear home can be used to secure:

- A bridge loan for your next purchase

- A business or investment loan

4. 🛠️ Renovate Without Red Tape

You’re free to start renovations right away without lender restrictions. Great for:

- Fix-and-flip buyers

- Custom remodels

- Buy-renovate-hold investors

5. 🏘️ Turn the Property into a Rental

With no mortgage, your rental income = higher cash flow. Some owners:

- Rent long-term or mid-term

- List on Airbnb or other platforms

- House hack with ADUs or roommates

6. 📜 Set Up a Living Trust or Estate Plan

Smart buyers immediately:

- Add the property to a trust

- Update wills or estate plans

- Consult with a CPA or estate attorney for protection and tax planning

7. 🛡️ Buy an Owner’s Title Insurance Policy

Even in a cash deal, this is optional, but highly recommended for long-term protection against title disputes or hidden liens.

8. 🧮 Adjust for Tax Implications

- Your property taxes will likely be reassessed based on purchase price.

- You won’t get mortgage interest deductions, but you may plan other deductions.

- High-net-worth buyers often restructure assets after buying a home all cash.

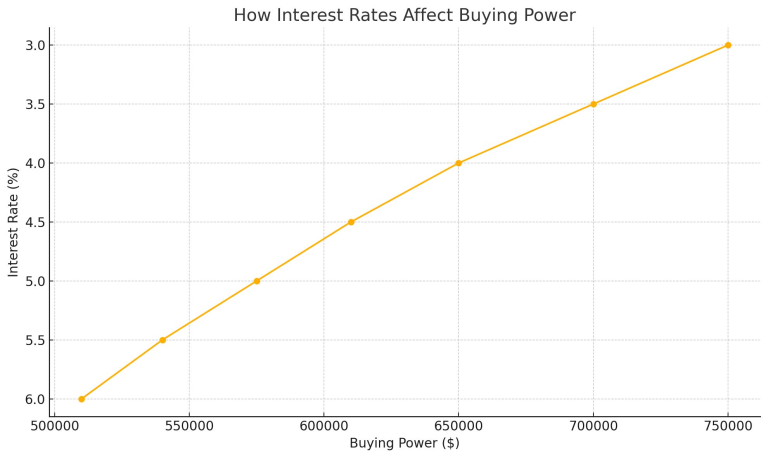

🧠 Is It Smart to Pay All Cash When Rates Are High?

Yes, when rates are high, avoiding a 7% mortgage can save tens of thousands.

When rates are low, it may be better to finance and invest the rest, especially if your money could earn more than the cost of borrowing.

🥈 What’s the Next Best Thing to an All-Cash Offer?

Not everyone has a suitcase of cash, and that’s okay. Here’s how to make your offer nearly as strong:

1. ✅ Fully Underwritten Loan Approval

Stronger than pre-approval. This means your lender has already verified everything. Sellers love it.

2. 🚫 Waive Loan Contingency (Carefully)

This removes the safety net if your loan falls through. Do this only with rock-solid financing.

3. 🕒 Shorten Contingency Periods

The faster you move, the more serious you look. Consider inspections within 5–7 days.

4. 💰 Make a Large Down Payment

30–50% down payments reduce lender friction and show financial strength.

🕓 Summary: Cash vs Financing Breakdown

| Feature | All-Cash Offer | Financed Offer |

|---|---|---|

| Loan Approval | ❌ Not Needed | ✅ Required |

| Appraisal | ❌ Optional | ✅ Required |

| Escrow Time | 7–14 Days | 30–45 Days |

| Contingencies | Optional | Often Required |

| Post-Close Strategy | HELOC, Refi, Trust | Mortgage Payoff |

| Title Insurance | Optional | Required by Lender |

| Liquidity | Tied Up | Preserved |

🎯 Final Thoughts: Should You Make an All-Cash Offer?

Paying all cash is powerful, and can put you in control of your home, your timing, and your terms.

But even after the keys are yours, there are smart moves you can make to put your equity to work or plan for the future.

If all cash isn’t an option, don’t worry, we can structure a strong, competitive offer with the next best tools available.

📞 Let’s Talk Strategy

Whether you’re buying with all cash, looking to unlock equity, or crafting a powerful offer with financing, I’m here to guide you. From Conejo Valley to West LA, let’s make your next move a smart one.